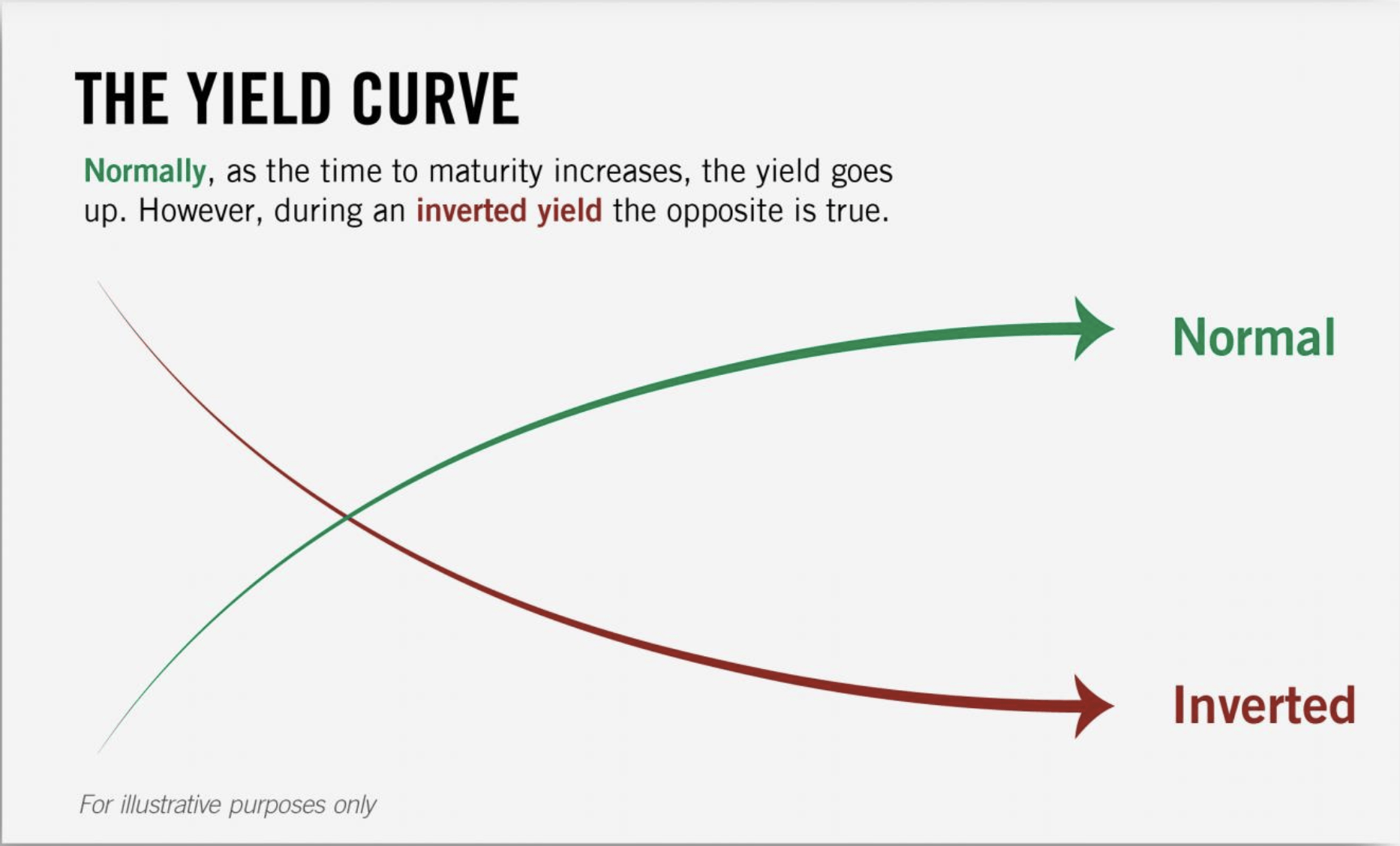

Does An Inverted Yield Curve Predict A Recession?

The movement in interest rates, the slope of the curve, and the absolute level of interest rates, do they matter when predicting a future economic slowdown?

The Academic Versus The Floor Trader

Artura Estrella is a respected, researcher and academic working with the Federal Reserve Bank of New York. He argues that in the 7 recessions since 1968, the 3 month/10 year spread, when inverted, correctly predicted the onset with 100% accuracy.

Rick Santelli, a former Drexel Burnham Lambert commodity trader, who has reported for CNBC from an exchange floor for the last 23 years, is respected for his practical knowledge and stylistic approach.

Being a trader at heart, Santelli while demonstrating a thorough understanding of Estrella’s work, argues that the 2yr/10yr spread provides similar information.

He very politely shows deference to the professor and reiterates that floor traders routinely overlay the 2yr/10yr and 3mo/10yr charts and find sticking similarities.

Traders believe that a partial inversion has predictive power but, what does a fully inverted yield curve suggest? Dr. Estrella warns that the formal, quantitative research was done on the 3 month/10 year spread and not to rely on unproven theory for fear of predicting 9 of the last 5 recessions.

What Is A Yield Spread? Is this time different?

The U.S. Treasury 3month/10 year Yield Spread Defined And Explained

Investopedia explains the “yield spread is the difference between yields on differing debt instruments of varying maturities, credit ratings, issuer, or risk level, calculated by deducting the yield of one instrument from the other. This difference is most often expressed in basis points (bps) or percentage points.”

When comparing the yields on U.S. Treasury securities the spread is known as the “yield spread”. When reviewing the spread on debt instruments of different issuers it is know as a credit spread. This makes intuitive sense as one is comparing non-similar bonds which may have different credit ratings and risk profiles.

An investor seeks to be compensated for taking on additional risk from either maturity (time to payoff), credit risk (likelihood of payoff), risk of inflation, and in comparison to investment in other asset classes.

Have Questions On Interest Rates, an inverted yield curve or the housing market? Speak With An Expert

If you would like to discuss any part of this post, please click through and let’s schedule a time to talk or leave a comment.